Most people, when they hear "mental wellness," think meditation apps, therapy, journaling, or sleep routines.

Almost nobody thinks: I need to fix my relationship with money.

Yet after 20 years coaching professionals through burnout, distraction, and stalled ambitions, I can tell you with confidence: financial chaos is one of the most reliably destructive forces against mental clarity I've ever seen. More insidious than poor sleep. More corrosive than constant notifications.

Because financial stress never clocks out.

The Connection Nobody Talks About

Mental wellness and personal finance seem like separate conversations. One belongs to the self-help section; the other to spreadsheets and advisors.

But in practice – inside the minds and lives of real people – they are deeply, stubbornly linked.

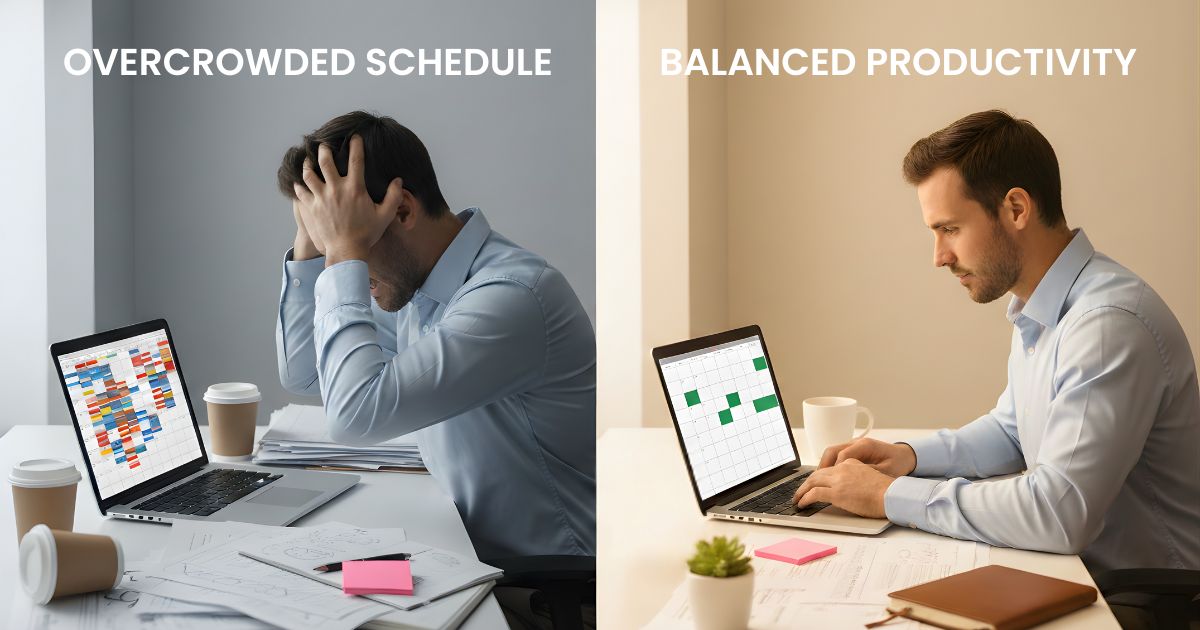

When your finances feel out of control, your nervous system stays on alert. When debt feels unmanageable, the background hum of low-grade anxiety never fully quiets. When you don't know exactly how much is in your account, or whether you'll cover next month's rent, your brain is never fully at rest – even when you're "not thinking about money."

The result? Less focus, less patience, worse decisions, and an emotional reserve that's chronically depleted.

This isn't weakness. It's neuroscience.

And – crucially – it's fixable with the right personal finance habits.

This Is Your Brain on Financial Stress

The Cognitive Bandwidth Tax

In 2013, a landmark study published in Science by Mani, Mullainathan, Shafir, and Zhao found something that stopped the behavioral economics world in its tracks.

Research from Princeton and Harvard demonstrated that financial worry – the persistent, low-grade anxiety of money scarcity – consumes cognitive bandwidth equivalent to a 13-point reduction in effective IQ. Not because poor people are less intelligent. Because their minds are occupied. The mental load of managing financial uncertainty leaves significantly less processing capacity for everything else: decisions, creativity, relationships, long-term planning.

Think about what that means in practice.

Every habit you're trying to build – better sleep, more deep focus, consistent fitness and exercise, a meditation and mindfulness practice – runs on the same cognitive and emotional fuel that financial stress is quietly burning through.

You're not struggling to build habits because you lack discipline. You're struggling because part of your operating system is perpetually occupied.

Debt, Anxiety, and the Mental Health Spiral

The relationship between personal finances and mental wellness isn't just about "feeling stressed." It's structural.

A systematic review and meta-analysis published in Clinical Psychology Review – covering 65 studies across multiple countries – found that personal unsecured debt is consistently associated with elevated rates of depression, anxiety disorders, and in severe cases, suicidal ideation. (Richardson, Elliott & Roberts, 2013)

The mechanism is vicious: financial stress raises cortisol, cortisol disrupts sleep, poor sleep degrades decision-making, bad decisions worsen the financial situation. A loop that feels impossible to exit from the inside.

But here's the thing no one tells you: you don't need to become wealthy to break this loop. You need to become more systematic.

The Earning-Building Gap: An Economist's Perspective

As an economist, I've spent decades watching people confuse income with financial security. They're not the same thing – and the difference is almost entirely behavioral.

You can earn well for 30 years and build nothing. The gap between earning and building isn't income. It isn't luck. It's habit.

Most professionals I've worked with don't have a revenue problem. They have a systems problem. Money arrives, and without a designed destination – savings automated before discretionary spending begins, expenses tracked before patterns become invisible – it leaves just as efficiently as it came.

This is what I mean by the earning-building gap: the invisible distance between what you make and what you accumulate, caused not by insufficient income, but by insufficient habit architecture.

The time allocation frameworks we use in productivity apply directly to money. Every dollar, like every hour, needs a default assignment – or it disappears into whatever feels urgent right now.

And unlike discretionary spending, the mental wellness returns from financial systems begin almost immediately. Not when you're rich. When you feel in control.

Your Financial Habit Stack: Five Boring, Powerful Moves

I'm not going to recommend stock portfolios or cryptocurrency strategies. I'm going to tell you what actually changed things for the clients I've coached – and for myself.

Track Every Expense for 30 Days

Awareness is the foundation of any habit system. Without knowing where your money goes, you're managing a budget blindfolded.

Use a simple spreadsheet, a notebook, or one of the tools in our personal finance category. Don't judge. Don't adjust yet. Just track. The patterns will surface on their own – and what you see will motivate action more than any advice I give you here.

Use the same time tracking mentality you'd apply to an audit of your calendar: you can't optimise what you haven't measured.

Automate One Saving Action

The single most effective personal finance intervention backed by behavioural research is automation. When saving requires willpower – a conscious, deliberate act every month – it competes with every other demand on your mental resources. When it's automatic, it sidesteps willpower entirely.

Set up an automatic transfer to a separate savings account on payday. Start with an amount small enough to be painless – 2%, $50, whatever doesn't break your current month. The amount matters less than the habit. You're building the architecture, not solving the math.

This is scheduling applied to money: you design the system once, and it runs without you.

Build a Starter Emergency Fund

This is the single financial habit with the highest return on mental wellness per euro or dollar invested.

Target one month of basic fixed expenses – rent, utilities, essential food. Nothing more ambitious yet. Even $500-1,000 sitting in a dedicated account dramatically reduces the cortisol response to financial uncertainty. It doesn't make you wealthy. It makes your nervous system stop treating every unexpected expense as a crisis.

One client – a talented, high-performing project manager – described crossing this threshold as "the first time in years I could actually think at work without part of my brain somewhere else." She hadn't changed her income. She'd changed her financial architecture.

Audit Your Subscriptions Monthly

Every month, spend 15 minutes reviewing what's leaving your account automatically. Most people are paying for between 2 and 5 services they no longer use. This isn't about frugality – it's about intentionality. The same attention you'd bring to protecting your calendar from meaningless meetings applies here.

Every subscription you cancel with clear intent reinforces a single, powerful identity: I make deliberate choices about where my resources go.

Dedicate 15 Minutes Per Week to a Financial Check-In

Avoidance is the primary driver of financial anxiety. When you don't look, the uncertainty expands to fill the mental space. When you look regularly – weekly, briefly, without judgment – the reality is almost always less frightening than the anxiety was.

This is your journaling practice for money. A short, consistent review: what came in, what went out, where you stand against your savings target. Use a habit tracking tool to maintain the streak and keep yourself accountable.

The goal isn't to solve every problem in 15 minutes. It's to keep financial clarity in your peripheral vision rather than your blind spot.

The Cascade Effect: When Money Habits Clean Up Everything Else

Here's what surprises every client who builds a basic financial system: the benefits bleed into everything.

Better financial clarity improves sleep – anxiety about money is one of the leading causes of nighttime rumination. It improves your capacity for deep focus – freed cognitive bandwidth goes somewhere. It supports mental wellness directly – the sense of agency that comes from a working financial system is its own form of psychological resilience.

It even tends to improve nutrition choices – financial stress is a documented driver of emotional eating and poor dietary decisions.

None of this requires a high income. All of it requires systems.

Explore the full range of connected tools and resources at BetterHabitsHub – 630+ curated tools across 21 categories, organised to support exactly this kind of habit cascade.

Frequently Asked Questions

Does personal finance actually affect mental health?

Yes, significantly. Research consistently shows that financial stress and personal debt are associated with higher rates of depression, anxiety, and cognitive impairment. The relationship works in both directions: financial stress worsens mental health, and poor mental health makes financial decisions harder. Building simple financial habits addresses both sides of this loop.

Do I need to earn more money to feel less financially stressed?

Not necessarily, and often not initially. The research on financial stress suggests that the feeling of control – clarity about what's coming in, where it's going, and what's set aside – reduces anxiety more reliably than income level alone. Basic systems: tracking, automation, and a small emergency buffer can shift your mental state significantly before your income changes at all.

What's the smallest financial habit I can start today?

Track every expense today. Just today. Not to judge or restrict – simply to see. This single act builds the awareness that makes every subsequent financial habit possible. Pair it with a habit tracking tool to maintain the daily momentum.

How does financial stress connect to other habit categories?

Financial stress is a cognitive bandwidth drain. When it's persistent, it reduces the mental and emotional resources available for every other habit – sleep, focus, exercise, and mindfulness all depend on having enough of yourself left to show up for them. Stabilising your financial foundation frees those resources.

Are there tools specifically for building financial habits?

Yes. The personal finance category at BetterHabitsHub includes curated tracking, budgeting, and savings tools selected for people building foundational money habits – not for advanced investors.

The Bottom Line

Mental wellness is not built in isolation from the real stresses of daily life.

You can meditate every morning and still lose an hour of productive focus to financial anxiety before noon. You can sleep eight hours and still wake up to a cortisol spike triggered by a bill you didn't open.

Financial health and emotional resilience are structurally connected. Building one strengthens the other.

The good news: the habits that close the gap are boring, small, and available to you today. You don't need a raise. You don't need a financial advisor. You need a system – and the willingness to start with one embarrassingly simple action.

Track one day's expenses. Set up one automatic transfer. Open the account statement you've been avoiding.

That's where financial confidence – and with it, mental clarity – actually begins.

Ready to Build Your Financial Foundation?

Join professionals who get weekly strategies on habits, finance, and tools that actually work.

👉 Subscribe to Our Newsletter – One email, once a week, zero fluff.

Or dive straight in:

→ Explore Personal Finance Tools – curated resources to start tracking, automating, and stabilising your finances

→ Browse Mental Wellness Tools – support the mind while you build the system

→ Start Tracking Your Habits – tools to keep your financial check-in streak alive

→ Discover All 630+ Tools – across 21 categories, built for people who want systems, not hype

There's no shortcut to financial peace of mind. There's only the habit of showing up – week after week, number after number.

--

— Mi Rad

PhD Economist & Business Coach